Peace of Mind from Using an Experienced Tax Team

When using Taxfile, you are using an experienced team that will make dealing with your tax affairs seamless. A lot of clients start by coming into our office stressed and overwhelmed, not knowing where to start. Using your current position and needs, we plan a step-by-step approach to keep you on top of your affairs and the relationship between you and HMRC harmonious. Once you are officially on board with us, we will have access to your HMRC record and, with our dedicated agent lines to HMRC, we’ll be able to speak to them on your behalf. This way, you are free from having to call them yourself and wait longer than we do for a call handler. You can also have any issues or queries explained to you in an easy to understand way by our friendly team. If you receive any letters that from HMRC and you don’t understand anything, we will be able to take a look for you and explain what it’s all about.

Any fee you pay Taxfile is tax deductible, so will be put on your tax return and result in a reduction of tax.

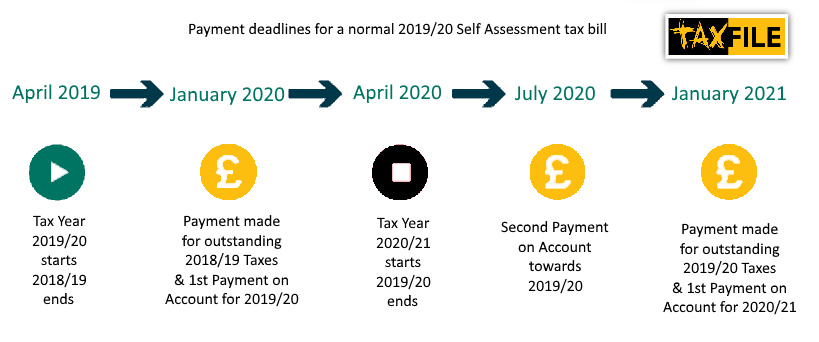

Our up-to-date knowledge of the tax system will give you peace of mind, alleviate any anxiety you may have and make the whole experience very different to how a lot of people find it when they are not using a team like ours. We know the best way to approach a tax situation that, without our experience and knowledge, could otherwise result in a lot more time and money being spent unnecessarily. From something as small as missing a tax return deadline, it can spiral into something a lot bigger, potentially including penalties, late payment interest, debt collection agencies being involved and so on. We inform all our clients of upcoming deadlines, for their particular tax situation, and let them know what needs doing and when, avoiding this situation and many more.

Unlike a lot of other companies, our tax experts and accountants are approachable, accessible and happy to help. We’re a unique tax advisor and accountancy practice like no other, with offices in Tulse Hill and Dulwich. We can help with any tax-related issues, including bookkeeping, filling in a tax return, limited company accounts, help accounting for property lettings, tax refunds and anything accountancy-related. Call Taxfile on 020 8761 8000, book a free 20-minute appointment with us (remote or in-person options available) or simply email us your tax-related query here.

This post was brought to you by Julie at Taxfile.