The Chancellor’s Autumn Budget 2017

This week, Chancellor of the Exchequer Philip Hammond delivered his Autumn Budget Statement to the House of Commons. View his full 1 hour speech in the official UK Parliament video below, which also includes a response from Jeremy Corbyn, leader of the opposition:

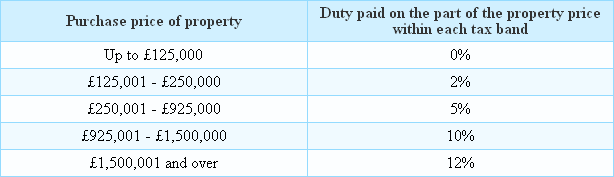

The biggest news from this budget was the Stamp Duty announcement, wherein first time buyers buying a property up to £300,000 in value will no longer pay Stamp Duty at all (saving £5k), nor pay it on the first £300,000 of homes costing up to £500,000. Money man Martin Lewis gave his take on the proposed Stamp Duty changes and answered frequently asked questions pertaining to exactly what defines a first time buyer in an interview on Good Morning Britain yesterday — here is a 5 minute clip:

Other winners included

- The Personal Allowance, which is the amount people can earn before they need to start paying income tax, is set to increase by £350 from £11,500 to £11,850 for those earning up to £100k per annum.

- The National Living Wage (NLW) will increase from £7.50 to £7.83 per hour from April 2018. This will affect UK workers aged over 25.

- The Chancellor promised investment of £160m in 5G mobile networks …

- … and a total of £550m for electric cars.

- He also set aside an additional £1.5 billion in Universal Credit to help those on benefits.

- £40m was set aside for a teacher training fund for under-performing schools in England.

- NHS England is to receive £2.8BN in investment (less, though, than the £4BN NHS bosses said is needed).

- From April 2018, the Consumer Price Index (CPI) is set to replace the Retail Price Index (RPI) as the inflation measure through which business rates will be calculated. It is anticipated that this change will save businesses £2.3BN in the first three years of the change.

- The Chancellor also abolished the very unpopular staircase tax and promised that those affected to date by the staircase tax would see original rates reinstated. Revaluations will take place every three years (previously five) after the next scheduled revaluation in 2022.

Losers included:

- The Chancellor revised down the growth forecasts for GDP, productivity growth and business investment.

- £3BN was set aside for helping to combat Brexit challenges.

- For second property owners, powers have been given to local authorities to charge a 100% council tax premium on empty houses. (See our note about those getting an income from property rental below).

If you have any questions about how the Autumn Budget might affect you, or any queries about any tax or accounting issues and requirements you may have, simply contact Taxfile on 0208 761 8000, send us a message here or book a 20 minute appointment online here and we’ll be happy to help. We also offer specific tax help and accounting for landlords so do get in touch if you would like to make sure you’re claiming no more and no less than you should if you’re getting an income from letting property.

Links to more detailed HMRC information about the Autumn Budget Statement can be read online here.